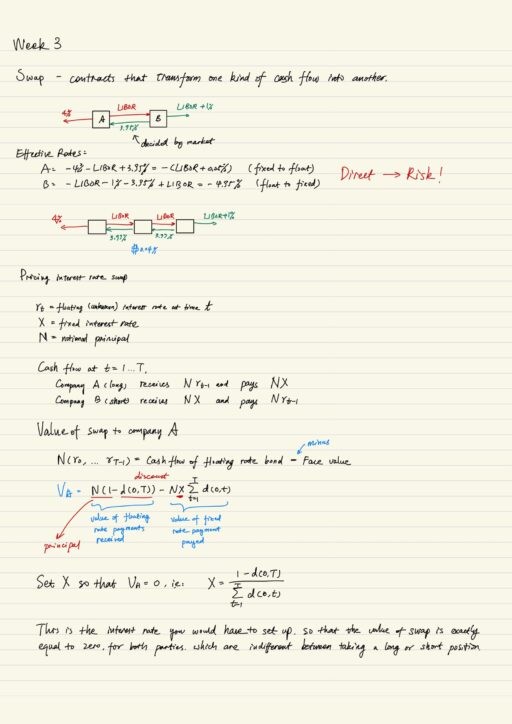

Financial Engineering and Risk Management Part IColumbia University An amazing course from a prestigious university! This course touches the hard core of various financial concepts by deriving numerous math equations. It effectively demonstrated why Financial Engineering is a multidisciplinary field drawing from economics, statistics, and engineering. It usually costs me a few hours to fully…